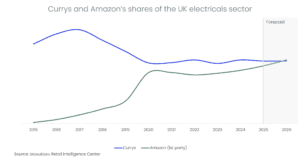

Currys is about to forfeit its top spot in the UK electricals sector to Amazon, with the online platform’s first party electricals sales set to exceed those of Currys by the end of 2026 (something its combined first and third party sales achieved some time ago). A competitive retail offering is central to Currys’ business model success, and the retailer must make the most of its store portfolio to compete effectively with the sheer convenience of Amazon’s proposition. Otherwise, its share of the electricals sector could fall behind the US retail giant as early as this year, says GlobalData, a leading intelligence and productivity platform.

To effectively compete with its online pureplay rivals, Currys must leverage its key point of difference: its stores. Currys must advocate for stores as essential for a superior customer experience and accessibility. Convenience is a key driver for electricals shoppers across all categories, so Currys must remove as many barriers as possible and make store visits worth the consumer’s while.

Oliver Maddison, senior retail analyst at GlobalData, comments: “While Currys has attempted to highlight the expertise of its staff in its marketing, it must emphasise this as part of a holistic customer service experience to help guide the customer through the breadth of choice available to find the product that best suits their needs.”

The stores must also be attractive places to spend time. GlobalData estimates that Currys’ instore B2C electricals sales declined by c.1% in 2025. Better visual merchandising, more accessible store locations, and better integration of online with instore customer service would encourage more footfall and drive sales both instore and online.

Maddison continues: “Currys must strike a careful balance. Its instore experience must enhance the shopping journey, adding value with experiential displays which provide shoppers with more information than they can find online. However, it must continue to make its online offering more competitive and user-friendly by offering more engaging comparison tools to allow consumers to compare its vast range on more than just specifications.”

Currys’ revenue growth in recent years has been primarily driven by its B2B operations and services. These revenue streams are worthy pursuits – services yield recurring revenues and higher margins, and Currys’ brand stands it in good stead to pick up B2B customers which AO has shifted away from – and have far outpaced its retail sales.

Maddison concludes: “Although services and B2B are delivering growth, neither is a valid substitute for a strong retail proposition. B2B relies on its retail brand and infrastructure, while product sales drive service sales. Currys also cannot rely on recurring services to remain a money-spinner. iD Mobile has been its golden goose, with its subscriber count growing 18% in Currys FY2025/26. However, it is soon to face heightened competition from rival specialist AO, online banking platform Monzo, and discount grocer Lidl.”